* feat(dashboard): apply Apple design system to all 4 pages

- Font: replace SF Pro with DM Sans (web-available) throughout

- Typography: consistent DM Sans stack, monospace data display

- ScreeningPanel: add horizontal scroll for mobile, fix stat card hover

- AnalysisMonitor: Apple progress bar, stage pills, decision badge

- BatchManager: add copy-to-clipboard for task IDs, fix error tooltip truncation, add CTA to empty state

- ReportsViewer: Apple-styled modal, search bar consistency

- Keyboard: add Escape to close modals

- CSS: progress bar ease-out, sidebar collapse button icon-only mode

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): secure API key handling and add stage progress streaming

- Pass ANTHROPIC_API_KEY via env dict instead of CLI args (P1 security fix)

- Add monitor_subprocess() coroutine with fcntl non-blocking reads

- Inject STAGE markers (analysts/research/trading/risk/portfolio) into script stdout

- Update task stage state and broadcast WebSocket progress at each stage boundary

- Add asyncio.Event for monitor cancellation on task completion/cancel

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* feat(dashboard): persist task state to disk for restart recovery

- Add TASK_STATUS_DIR for task state JSON files

- Lifespan startup: restore task states from disk

- Task completion/failure: write state to disk

- Task cancellation: delete persisted state

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): correct stage key mismatch, add created_at, persist cancelled tasks

- Fix ANALYSIS_STAGES key 'trader' → 'trading' to match backend STAGE markers

- Add created_at field to task state at creation, sort list_tasks by it

- Persist task state before broadcast in cancel path (closes restart race)

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* feat(dashboard): add portfolio panel - watchlist, positions, and recommendations

New backend:

- api/portfolio.py: watchlist CRUD, positions with live P&L, recommendations

- POST /api/portfolio/analyze: batch analysis of watchlist tickers

- GET /api/portfolio/positions: live price from yfinance + unrealized P&L

New frontend:

- PortfolioPanel.jsx with 3 tabs: 自选股 / 持仓 / 今日建议

- portfolioApi.js service

- Route /portfolio (keyboard shortcut: 5)

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* feat(dashboard): add CSV and PDF report export

- GET /api/reports/export: CSV with ticker,date,decision,summary

- GET /api/reports/{ticker}/{date}/pdf: PDF via fpdf2 with DejaVu fonts

- ReportsViewer: CSV export button + PDF export in modal footer

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): address 4 critical issues found in pre-landing review

1. main.py: move API key validation before task state creation —

prevents phantom "running" tasks when ANTHROPIC_API_KEY is missing

2. portfolio.py: make get_positions() async and fetch yfinance prices

concurrently via run_in_executor — no longer blocks event loop

3. portfolio.py: add fcntl.LOCK_EX around all JSON read-modify-write

operations on watchlist.json and positions.json — eliminates TOCTOU

lost-write races under concurrent requests

4. main.py: use tempfile.mkstemp with mode 0o600 instead of world-

readable /tmp/analysis_{task_id}.py — script content no longer

exposed to other users on shared hosts

Also: remove unused UploadFile/File imports, undefined _save_to_cache

function, dead code in _delete_task_status, and unused

get_or_create_default_account helper.

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): use secure temp file for batch analysis scripts

Batch portfolio analysis was writing scripts to /tmp with default

permissions (0o644), exposing the API key to other local users.

Switch to tempfile.mkstemp + chmod 0o600, matching the single-analysis

pattern. Also fix cancel_task cleanup to use glob patterns for

tempfile-generated paths.

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): remove fake fallback data from ReportsViewer

ReportsViewer showed fabricated Chinese text when a report failed to load,

making fake data appear indistinguishable from real analysis. Now shows

an error message instead.

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix(dashboard): reliability fixes - cross-platform PDF fonts, API timeouts, yfinance concurrency, retry logic

- PDF: try multiple DejaVu font paths (macOS + Linux) instead of hardcoded macOS

- Frontend: add 15s AbortController timeout to all API calls + proper error handling

- yfinance: cap concurrent price fetches at 5 via asyncio.Semaphore

- Batch analysis: retry failed stock analyses up to 2x with exponential backoff

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

* fix: resolve 4 critical security/correctness bugs in web dashboard

1. Mass position deletion (portfolio.py): remove_position now rejects

empty position_id — previously position_id="" matched all positions

and deleted every holding for a ticker across ALL accounts.

2. Path traversal in get_recommendation (portfolio.py): added ticker/date

validation (no ".." or path separators) + resolved-path check against

RECOMMENDATIONS_DIR to prevent ../../etc/passwd attacks.

3. Path traversal in get_report_content (main.py): same ticker/date

validation + resolved-path check against get_results_dir().

4. china_data import stub (interface.py + new china_data.py): the actual

akshare implementation lives in web_dashboard/backend/china_data.py

(different package); tradingagents/dataflows/china_data.py was missing

entirely, so _china_data_available was always False. Added stub file

and AttributeError to the import exception handler so the module

gracefully degrades instead of silently hiding the missing vendor.

Magic numbers also extracted to named constants:

- MAX_RETRY_COUNT, RETRY_BASE_DELAY_SECS (main.py)

- MAX_CONCURRENT_YFINANCE_REQUESTS (portfolio.py)

Co-Authored-By: Claude Opus 4.6 <noreply@anthropic.com>

---------

Co-authored-by: Claude Opus 4.6 <noreply@anthropic.com>

|

||

|---|---|---|

| assets | ||

| cli | ||

| tests | ||

| tradingagents | ||

| web_dashboard | ||

| .dockerignore | ||

| .env.example | ||

| .gitignore | ||

| Dockerfile | ||

| LICENSE | ||

| README.md | ||

| docker-compose.yml | ||

| main.py | ||

| pyproject.toml | ||

| requirements.txt | ||

| test.py | ||

| uv.lock | ||

README.md

TradingAgents: Multi-Agents LLM Financial Trading Framework

News

- [2026-03] TradingAgents v0.2.3 released with multi-language support, GPT-5.4 family models, unified model catalog, backtesting date fidelity, and proxy support.

- [2026-03] TradingAgents v0.2.2 released with GPT-5.4/Gemini 3.1/Claude 4.6 model coverage, five-tier rating scale, OpenAI Responses API, Anthropic effort control, and cross-platform stability.

- [2026-02] TradingAgents v0.2.0 released with multi-provider LLM support (GPT-5.x, Gemini 3.x, Claude 4.x, Grok 4.x) and improved system architecture.

- [2026-01] Trading-R1 Technical Report released, with Terminal expected to land soon.

🎉 TradingAgents officially released! We have received numerous inquiries about the work, and we would like to express our thanks for the enthusiasm in our community.

So we decided to fully open-source the framework. Looking forward to building impactful projects with you!

🚀 TradingAgents | ⚡ Installation & CLI | 🎬 Demo | 📦 Package Usage | 🤝 Contributing | 📄 Citation

TradingAgents Framework

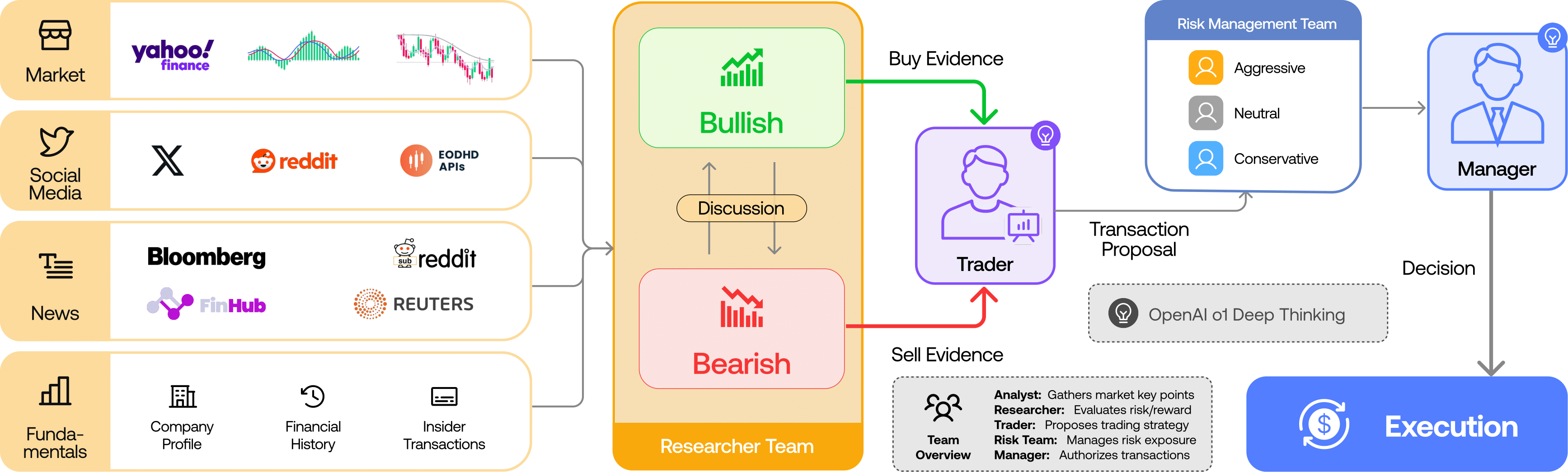

TradingAgents is a multi-agent trading framework that mirrors the dynamics of real-world trading firms. By deploying specialized LLM-powered agents: from fundamental analysts, sentiment experts, and technical analysts, to trader, risk management team, the platform collaboratively evaluates market conditions and informs trading decisions. Moreover, these agents engage in dynamic discussions to pinpoint the optimal strategy.

TradingAgents framework is designed for research purposes. Trading performance may vary based on many factors, including the chosen backbone language models, model temperature, trading periods, the quality of data, and other non-deterministic factors. It is not intended as financial, investment, or trading advice.

Our framework decomposes complex trading tasks into specialized roles. This ensures the system achieves a robust, scalable approach to market analysis and decision-making.

Analyst Team

- Fundamentals Analyst: Evaluates company financials and performance metrics, identifying intrinsic values and potential red flags.

- Sentiment Analyst: Analyzes social media and public sentiment using sentiment scoring algorithms to gauge short-term market mood.

- News Analyst: Monitors global news and macroeconomic indicators, interpreting the impact of events on market conditions.

- Technical Analyst: Utilizes technical indicators (like MACD and RSI) to detect trading patterns and forecast price movements.

Researcher Team

- Comprises both bullish and bearish researchers who critically assess the insights provided by the Analyst Team. Through structured debates, they balance potential gains against inherent risks.

Trader Agent

- Composes reports from the analysts and researchers to make informed trading decisions. It determines the timing and magnitude of trades based on comprehensive market insights.

Risk Management and Portfolio Manager

- Continuously evaluates portfolio risk by assessing market volatility, liquidity, and other risk factors. The risk management team evaluates and adjusts trading strategies, providing assessment reports to the Portfolio Manager for final decision.

- The Portfolio Manager approves/rejects the transaction proposal. If approved, the order will be sent to the simulated exchange and executed.

Installation and CLI

Installation

Clone TradingAgents:

git clone https://github.com/TauricResearch/TradingAgents.git

cd TradingAgents

Create a virtual environment in any of your favorite environment managers:

conda create -n tradingagents python=3.13

conda activate tradingagents

Install the package and its dependencies:

pip install .

Docker

Alternatively, run with Docker:

cp .env.example .env # add your API keys

docker compose run --rm tradingagents

For local models with Ollama:

docker compose --profile ollama run --rm tradingagents-ollama

Required APIs

TradingAgents supports multiple LLM providers. Set the API key for your chosen provider:

export OPENAI_API_KEY=... # OpenAI (GPT)

export GOOGLE_API_KEY=... # Google (Gemini)

export ANTHROPIC_API_KEY=... # Anthropic (Claude)

export XAI_API_KEY=... # xAI (Grok)

export OPENROUTER_API_KEY=... # OpenRouter

export ALPHA_VANTAGE_API_KEY=... # Alpha Vantage

For local models, configure Ollama with llm_provider: "ollama" in your config.

Alternatively, copy .env.example to .env and fill in your keys:

cp .env.example .env

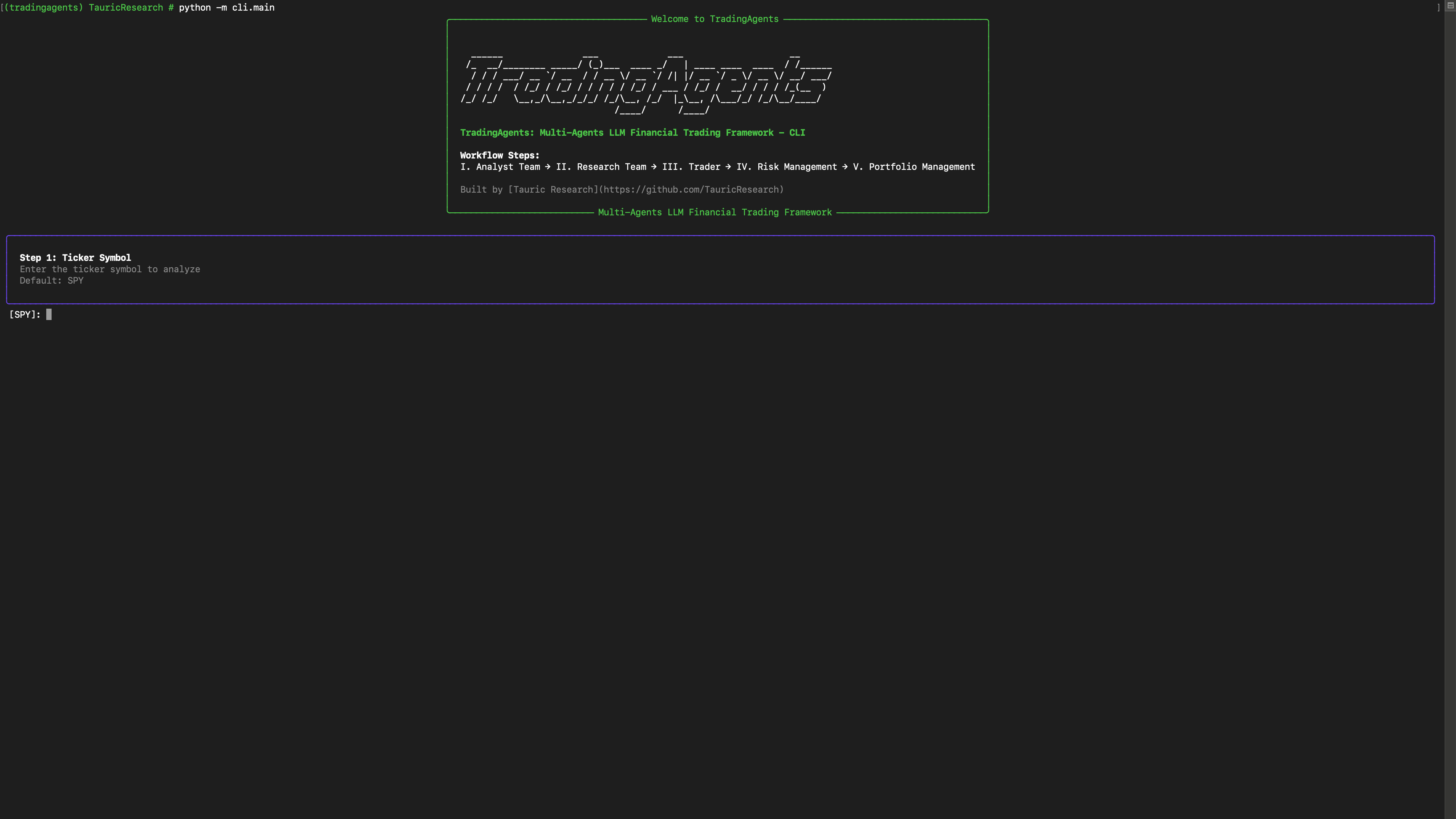

CLI Usage

Launch the interactive CLI:

tradingagents # installed command

python -m cli.main # alternative: run directly from source

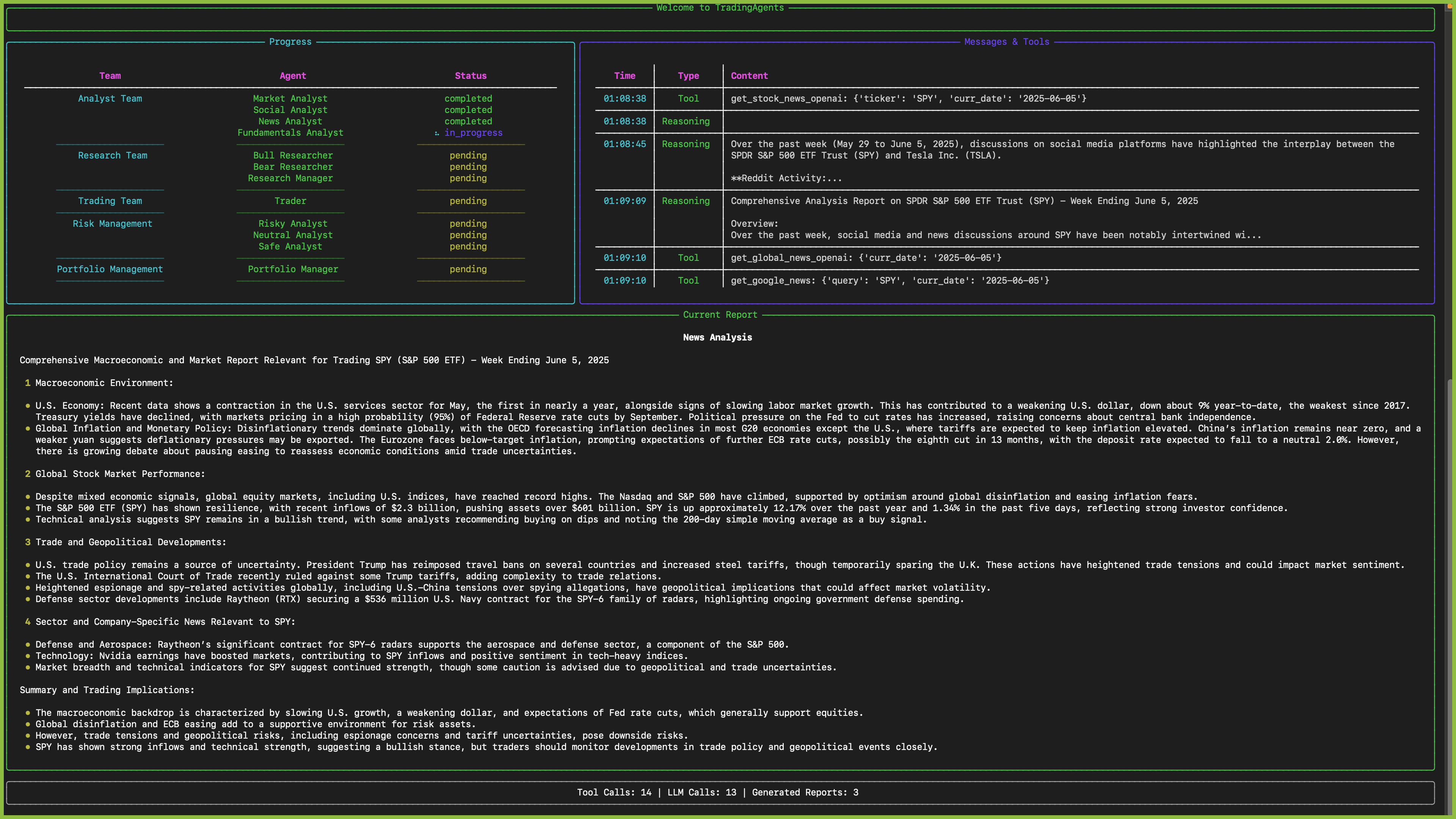

You will see a screen where you can select your desired tickers, analysis date, LLM provider, research depth, and more.

An interface will appear showing results as they load, letting you track the agent's progress as it runs.

![]()

TradingAgents Package

Implementation Details

We built TradingAgents with LangGraph to ensure flexibility and modularity. The framework supports multiple LLM providers: OpenAI, Google, Anthropic, xAI, OpenRouter, and Ollama.

Python Usage

To use TradingAgents inside your code, you can import the tradingagents module and initialize a TradingAgentsGraph() object. The .propagate() function will return a decision. You can run main.py, here's also a quick example:

from tradingagents.graph.trading_graph import TradingAgentsGraph

from tradingagents.default_config import DEFAULT_CONFIG

ta = TradingAgentsGraph(debug=True, config=DEFAULT_CONFIG.copy())

# forward propagate

_, decision = ta.propagate("NVDA", "2026-01-15")

print(decision)

You can also adjust the default configuration to set your own choice of LLMs, debate rounds, etc.

from tradingagents.graph.trading_graph import TradingAgentsGraph

from tradingagents.default_config import DEFAULT_CONFIG

config = DEFAULT_CONFIG.copy()

config["llm_provider"] = "openai" # openai, google, anthropic, xai, openrouter, ollama

config["deep_think_llm"] = "gpt-5.4" # Model for complex reasoning

config["quick_think_llm"] = "gpt-5.4-mini" # Model for quick tasks

config["max_debate_rounds"] = 2

ta = TradingAgentsGraph(debug=True, config=config)

_, decision = ta.propagate("NVDA", "2026-01-15")

print(decision)

See tradingagents/default_config.py for all configuration options.

Contributing

We welcome contributions from the community! Whether it's fixing a bug, improving documentation, or suggesting a new feature, your input helps make this project better. If you are interested in this line of research, please consider joining our open-source financial AI research community Tauric Research.

Citation

Please reference our work if you find TradingAgents provides you with some help :)

@misc{xiao2025tradingagentsmultiagentsllmfinancial,

title={TradingAgents: Multi-Agents LLM Financial Trading Framework},

author={Yijia Xiao and Edward Sun and Di Luo and Wei Wang},

year={2025},

eprint={2412.20138},

archivePrefix={arXiv},

primaryClass={q-fin.TR},

url={https://arxiv.org/abs/2412.20138},

}